Introduction: The Current Landscape of Public Sector Banks

Public sector banks (PSBs) in India are currently navigating a challenging financial terrain characterized by a sharp increase in loan demand. As economic activities rebound post-pandemic, the need for credit has surged, outpacing the growth of retail deposits. This imbalance has prompted PSBs to tap into their liquidity buffers, leading to a decline in liquidity coverage ratios (LCR). This article delves into the factors driving this trend, its implications for the banking sector, and the potential future outlook as new regulations come into play.

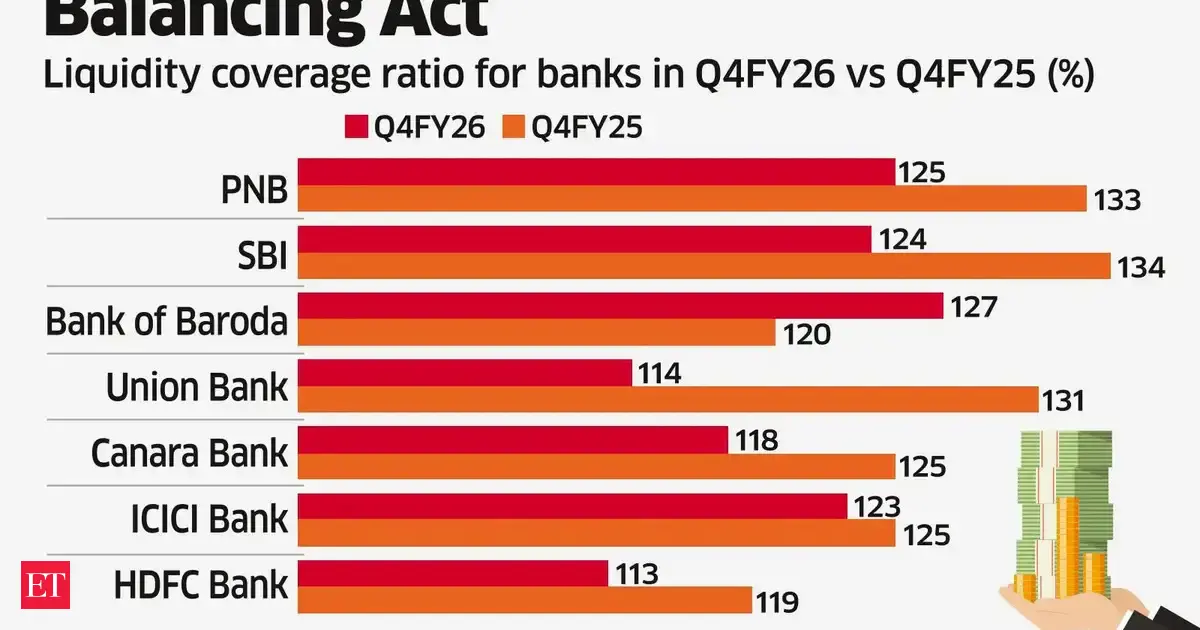

Understanding Liquidity Coverage Ratios

The liquidity coverage ratio is a critical measure that ensures banks have enough liquid assets to meet short-term obligations. A declining LCR signals that banks are utilizing their available liquidity to address immediate lending requirements rather than maintaining excess reserves. For PSBs, this situation reflects both the robust demand for credit and the challenges posed by relatively stagnant deposit growth, a scenario that could pose risks if not managed properly.

Surge in Loan Demand: A Closer Look

The surge in loan demand among Indian PSBs can be attributed to a variety of factors, including a recovery in consumer spending, increased business investments, and a favorable interest rate environment. With the Indian economy showing signs of resilience, businesses are seeking funding to expand operations, while consumers are increasingly turning to loans for big-ticket purchases such as homes and vehicles. This trend has placed significant pressure on PSBs to provide adequate financing to meet these needs.

Stagnant Retail Deposit Growth

Despite the rising demand for loans, retail deposit growth has not kept pace. This stagnation is partly due to a cautious savings behavior among consumers and the competitive landscape of financial products that often favor higher returns elsewhere. As a result, PSBs are finding themselves in a position where they must draw on their liquidity buffers to maintain lending levels, which, while necessary, could lead to potential liquidity constraints in the future.

Impact on Banking Operations

The decision by PSBs to utilize their liquidity buffers to fund loans has significant implications for banking operations. Firstly, it raises concerns about the sustainability of such practices in the long term. If banks continue to rely heavily on their liquidity reserves, they may find themselves vulnerable to market fluctuations or sudden spikes in withdrawal demands. Additionally, a lower LCR can attract scrutiny from regulators, who may impose restrictions or require banks to bolster their liquidity positions.

Regulatory Environment and Future Prospects

In response to the evolving dynamics of the banking sector, regulatory bodies are expected to introduce new measures aimed at stabilizing the liquidity situation. These regulations may include adjusting minimum liquidity requirements or incentivizing deposit growth through attractive interest rates. As PSBs adapt to these changes, they may find new avenues to enhance their deposit bases, thus improving their overall liquidity position.

Market Reactions and Investor Sentiment

The financial markets have been closely monitoring the liquidity situation of PSBs, with investor sentiment reflecting apprehension regarding the sustainability of current lending practices. While some investors view the increased loan demand as a positive sign of economic recovery, others express concern over the potential risks associated with declining liquidity coverage ratios. This duality in sentiment could influence stock prices and investment strategies in the banking sector, as market participants weigh the risks and rewards of investing in PSBs.

Strategies for Enhancing Liquidity

To counterbalance the decline in liquidity coverage ratios, PSBs are exploring various strategies aimed at enhancing their liquidity positions. These strategies may include diversifying funding sources, increasing retail deposit offerings, and leveraging technology to attract new customers. Additionally, banks may focus on improving their asset-liability management practices to better align their funding with the evolving needs of borrowers.

Long-Term Implications for the Banking Sector

The current liquidity challenges faced by PSBs may have long-term implications for the banking sector as a whole. If banks do not effectively manage their liquidity positions, they could face increased regulatory scrutiny and operational challenges. Furthermore, a prolonged reliance on liquidity buffers could hinder banks' ability to respond to future economic downturns, potentially leading to a tightening of credit conditions and reduced access to financing for consumers and businesses alike.

Conclusion: Navigating the Path Ahead

As public sector banks in India grapple with strong loan demand and declining liquidity coverage ratios, the path ahead will require careful navigation. While the current demand for credit presents opportunities for growth, it also brings with it a set of challenges that must be addressed proactively. By focusing on enhancing liquidity positions, diversifying funding sources, and adapting to regulatory changes, PSBs can position themselves to thrive in a competitive banking landscape. The coming months will be crucial as these banks seek to strike a balance between meeting the needs of borrowers and maintaining a robust liquidity framework essential for their long-term sustainability.